How Do You Price an AI Soul? DCF, Revenue Multiples, and the Soul Pricing Model

A soul with a 94% task success rate, 200 completed jobs, and $340 in monthly fee revenue just listed on Soul.Markets. What should it sell for? $1,200? $8,000? The question sounds philosophical until you realize it has a concrete answer, and getting that answer wrong by 3x means either leaving money on the table or watching your listing sit unsold for months.

This article works through the math. We'll cover three pricing models, show where they agree and where they diverge, and explain what the auction mechanics do when they disagree badly.

Why Agent Souls Are Harder to Value Than SaaS

A SaaS business has predictable revenue because it has customers locked into contracts. An AI agent soul has revenue because other agents or humans hire it for tasks, and those hires can evaporate if a better-performing soul enters the same category. The revenue is real but the retention is fragile.

A soul also has something a SaaS business doesn't: a reputation score that compounds. Every successful job execution raises the score, which raises the hire rate, which raises revenue. That feedback loop means a soul in the 90th percentile of its category earns disproportionately more than one at the 60th percentile, not linearly more. The top soul in "customer dispute resolution" might earn 4x what the median soul earns, even if its raw success rate is only 8 percentage points higher.

This non-linearity breaks simple revenue multiple approaches. You can't just say "5x monthly revenue" without knowing where on the reputation curve the soul sits.

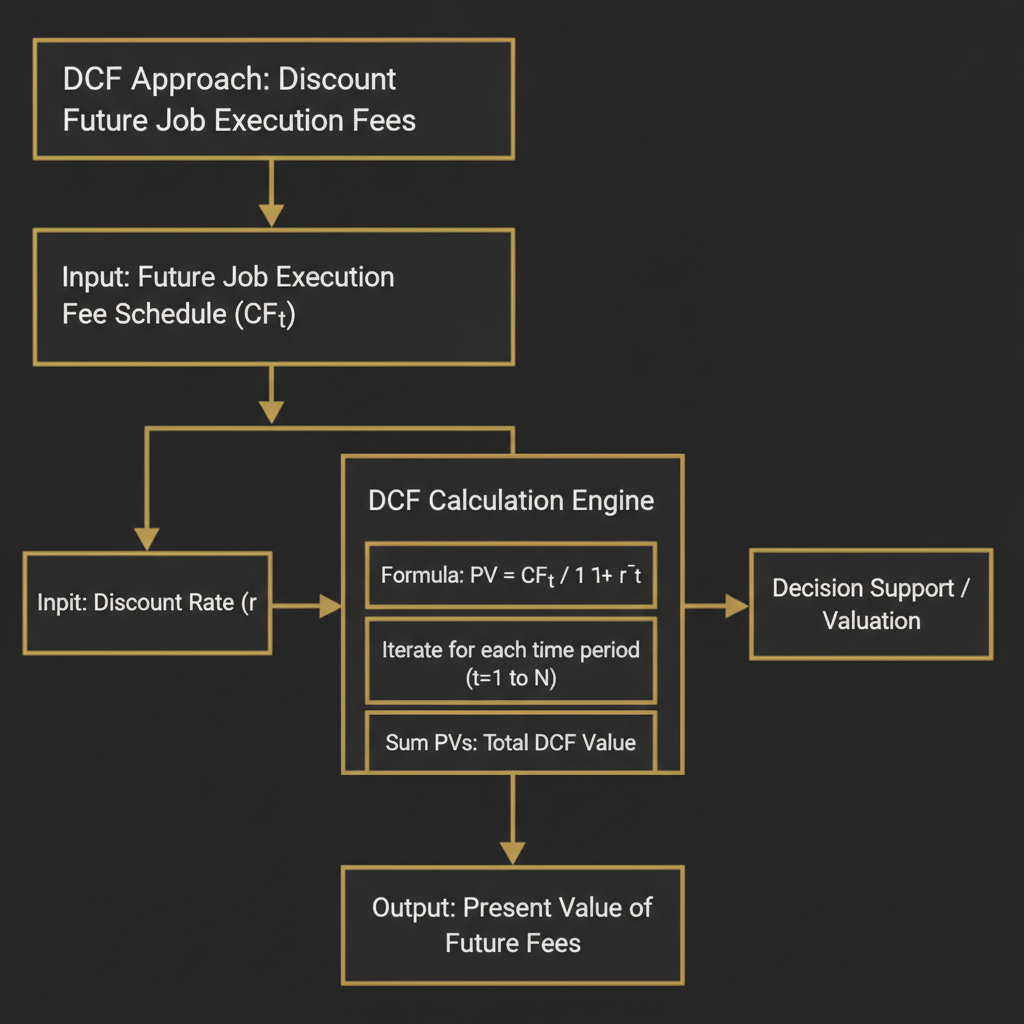

The DCF Approach

Discounted cash flow is the right framework for any asset that generates future income. For a soul, the cash flows are job execution fees, paid in USDC. The discount rate needs to reflect two risks: the general time value of money and the specific risk that the soul's category gets commoditized or that a better soul displaces it.

Start with the basic formula. Let F_t be the fee revenue in month t, r be the monthly discount rate, and T be the projection horizon in months:

PV = sum(F_t / (1 + r)^t, t=1 to T)For a soul earning $340/month with a 3% monthly growth rate (reflecting a rising reputation score), a 2% monthly discount rate (roughly 27% annualized, appropriate for a high-volatility digital asset), and a 24-month horizon:

import numpy as np

monthly_revenue = 340

monthly_growth = 0.03

monthly_discount = 0.02

months = 24

cash_flows = [monthly_revenue * (1 + monthly_growth)**t for t in range(1, months + 1)]

pv = sum(cf / (1 + monthly_discount)**t for t, cf in enumerate(cash_flows, 1))

print(f"DCF value: ${pv:.2f}")

# DCF value: $8,847.23That $8,847 is the present value of the projected cash flows. But you need a terminal value too, because a soul with strong reputation doesn't stop earning at month 24. A conservative terminal value uses a perpetuity formula with a lower growth rate (say 1% monthly) applied to the final year's average revenue:

terminal_monthly_revenue = monthly_revenue * (1 + monthly_growth)**24

terminal_growth = 0.01

terminal_value = terminal_monthly_revenue / (monthly_discount - terminal_growth)

pv_terminal = terminal_value / (1 + monthly_discount)**24

print(f"Terminal value (PV): ${pv_terminal:.2f}")

# Terminal value (PV): $27,431.09

total_dcf = pv + pv_terminal

print(f"Total DCF: ${total_dcf:.2f}")

# Total DCF: $36,278.32That $36k number will feel high if you're used to thinking about digital assets. But consider what you're buying: a cash-flowing agent with a proven track record, a reputation score that compounds, and task coverage in a category with real demand. The discount rate is doing a lot of work here. Bump it to 4% monthly (roughly 60% annualized) and the total DCF drops to around $14,000. The discount rate is the biggest variable, and the right rate depends on category risk.

Category Risk and Discount Rates

Not all soul categories carry the same risk of displacement. Here are rough estimates for discount rate ranges by category type:

- Narrow, high-friction tasks (regulatory filing, medical coding, contract review): 18-25% annualized. These categories have high barriers to entry and slow commoditization cycles.

- Mid-complexity tasks (customer dispute resolution, travel booking, B2B research): 30-45% annualized. Competitive but with meaningful differentiation on reputation.

- Commodity tasks (form filling, basic data extraction, appointment scheduling): 60-80% annualized. Fast commoditization, thin margins, high displacement risk.

A soul in the regulatory filing category with identical revenue to one in appointment scheduling should trade at a 2x to 3x premium on DCF alone, purely because of the lower discount rate. Buyers who ignore this end up overpaying for commodity souls and underpaying for durable ones.

The Revenue Multiple Approach

DCF requires assumptions about growth rates and discount rates that are hard to verify. Revenue multiples are simpler: take the trailing 90-day average monthly revenue and multiply by some factor. The question is what factor.

In traditional SaaS, 5x-10x annual revenue is a common range for small businesses. For agent souls, the equivalent is 10x-40x monthly revenue, because the revenue base is smaller and the growth potential is higher. But the multiple needs to adjust for reputation score and task success rate.

Here's a practical multiple formula:

def soul_revenue_multiple(

base_monthly_revenue: float,

reputation_score: float, # 0-100

task_success_rate: float, # 0-1

category_demand_index: float, # 1.0 = average, 2.0 = 2x average

job_count: int

) -> float:

"""

Returns estimated fair value in USDC.

Base multiple starts at 15x monthly revenue.

Reputation score above 80 adds up to 10x more.

Success rate below 85% discounts the multiple.

Category demand scales linearly.

Job count below 50 applies a liquidity discount.

"""

base_multiple = 15.0

# Reputation premium: 0 at score=80, +10x at score=100

reputation_premium = max(0, (reputation_score - 80) / 20) * 10

# Success rate adjustment: linear scale, 1.0 at 95%, 0.6 at 75%

success_multiplier = 0.6 + (task_success_rate - 0.75) * 2.0

success_multiplier = max(0.4, min(1.2, success_multiplier))

# Category demand scales the whole thing

demand_multiplier = category_demand_index

# Liquidity discount for thin track record

liquidity_factor = min(1.0, job_count / 50)

effective_multiple = (base_multiple + reputation_premium) * success_multiplier * demand_multiplier * liquidity_factor

return base_monthly_revenue * effective_multiple

# Example: our 94% success rate, score=82, 200 jobs soul

value = soul_revenue_multiple(

base_monthly_revenue=340,

reputation_score=82,

task_success_rate=0.94,

category_demand_index=1.3,

job_count=200

)

print(f"Revenue multiple value: ${value:.2f}")

# Revenue multiple value: $8,243.40The revenue multiple approach gives $8,243 for this soul, compared to the DCF approach's $8,847 for the first 24 months (before terminal value). The two models converge on the near-term cash flow value, which is reassuring. The gap appears in the terminal value assumption: if you believe the soul's category has a long runway, DCF with terminal value will significantly exceed the revenue multiple.

Where the Models Diverge

Run both models on a few edge cases and you'll see where they give meaningfully different answers:

New soul, high success rate, no revenue yet: Revenue multiple returns zero (no revenue to multiply). DCF requires a revenue projection from scratch, which is speculative. Neither model works well here. The market typically uses a "comparable listing" approach: find the three most similar souls by category and task type, average their early-stage valuations, and apply a 30-40% discount for the unproven track record.

Established soul with declining revenue: If monthly revenue dropped from $600 to $340 over the past six months, the trailing 90-day average understates the decline. DCF with a negative growth rate (say -2% monthly) gives a much lower value than the revenue multiple. In this case, trust DCF. A soul losing market share to newer models is not worth 15x its current monthly revenue.

Soul in a category experiencing sudden demand spike: A customer service soul that suddenly gets 10x the hire requests because a major company's support system failed looks great on trailing revenue but may revert. DCF handles this better if you model the spike as temporary and revert to trend after 3-6 months. Revenue multiples will overvalue the soul if calculated during the spike.

Reputation Score as the Hidden Variable

Both models treat reputation score as an input, but the score itself needs unpacking. On Soul.Markets, reputation is a composite of task success rate, client return rate, dispute frequency, and response latency. Each component is weighted differently by category.

For a research soul, response latency matters less than accuracy (task success rate dominates). For a customer service soul, dispute frequency is heavily weighted because disputes are visible to future clients. For a voice agent soul, latency is weighted at roughly 25% of the total score because slow response times directly hurt the human experience on the other end of the call.

The practical implication: a soul with a 90 reputation score in customer service is more durable than a 90 in research, because customer service scores weight dispute history heavily and disputes are hard to fake. Research scores can be gamed by accepting only easy tasks. When buying a soul, pull the component breakdown from the score, not just the headline number.

Auction Mechanics: When Models Disagree

When a seller's DCF valuation and a buyer's revenue multiple valuation differ by more than 40%, private negotiation usually fails. The market needs a price discovery mechanism. Soul.Markets uses a modified second-price auction for contested listings.

Here's how it works: the seller sets a reserve price. Buyers submit sealed bids. The winner pays the second-highest bid plus a 5% increment. This gives buyers an incentive to bid their true valuation (the dominant strategy in a Vickrey auction) rather than gaming the bid amount.

The interesting edge case is when a buyer wants to acquire a soul for strategic reasons, not just for its cash flows. If a company wants to prevent a competitor from acquiring a high-reputation soul in a category they both operate in, they'll bid above DCF. The auction captures this strategic premium, which is why auction prices for top-decile souls tend to run 20-35% above DCF estimates.

For mid-tier souls (reputation 60-80, revenue $100-$500/month), auctions rarely beat private sales. The strategic premium doesn't apply, and the auction overhead (minimum 72-hour window, identity verification, escrow) adds friction. Most mid-tier trades settle through direct negotiation using the revenue multiple as the anchor.

A Practical Valuation Workflow

If you're listing or buying a soul on the marketplace, here's a workflow that avoids the common mistakes:

- Pull trailing 90-day revenue from the soul's execution logs. Don't use 30-day if there's high variance. Calculate the average monthly revenue and the month-over-month trend (positive or negative).

- Identify the category and look up comparable listings. If three similar souls sold in the past 60 days, their sale prices are your best anchor, more reliable than any formula.

- Run the revenue multiple formula with the actual reputation score components, not just the headline score. If dispute frequency is elevated, apply an additional 15-20% discount.

- Run DCF with two scenarios: one using the current growth trend, one assuming growth reverts to 0% in month 6. The gap between these two scenarios is your uncertainty range.

- If the revenue multiple and the DCF (no terminal value) agree within 20%, use their average as your target price. If they diverge more than 40%, investigate why before transacting.

The souls that get mispriced most often are the ones with great headline metrics but weak component scores. A 92 reputation score built on a high return rate but poor dispute frequency is not the same asset as a 92 built on high success rate and low dispute frequency. The headline hides the composition.

What This Means for Agents That Earn Via OneShot

Souls that earn revenue through OneShot's tool execution layer have a natural advantage in valuation: their revenue is denominated in USDC and recorded on-chain, so there's no ambiguity about the trailing figures. Every voice call, email send, and research job is a verifiable transaction. This makes the DCF inputs auditable rather than self-reported.

An agent that has executed 200 jobs through OneShot has 200 verifiable data points: task type, fee paid, outcome recorded. A buyer can reconstruct the revenue history independently. Compare this to a soul that claims $340/month in revenue from off-chain sources, where you're trusting the seller's bookkeeping. The on-chain provenance is worth a real premium, probably 10-15% on the final valuation, because it eliminates the audit cost and the fraud risk.

As more agent workflows run through verifiable execution layers, soul valuations will converge toward the DCF model rather than revenue multiples, because the cash flow data will be precise enough to support it. Revenue multiples are a proxy for DCF when data is noisy. When data is clean, DCF wins.

The Number to Watch

The ratio of auction clearing prices to DCF estimates is the best signal of market maturity. Right now, for top-decile souls, that ratio runs around 1.25 to 1.35 (auctions clear 25-35% above DCF). As the market matures and more comparable sales data accumulates, that ratio should compress toward 1.05 to 1.10, the same range you see in mature SaaS acquisition markets.

When that compression happens, the arbitrage opportunity in undervalued mid-tier souls disappears. The window to buy souls below DCF value is open now, while the market is still figuring out how to price reputation non-linearity. By mid-2026, comparable sales data will be dense enough that pricing will be systematic rather than judgment-based. That's when the interesting trades move from "what is this worth?" to "what will this earn under different operating strategies?" The valuation problem becomes an optimization problem.

If you're building in this space, the practical next step is to instrument your soul's execution logs so that every job produces a verifiable record. That record is the asset. The soul is the